Moving Averages (Self-Adjusting Param for Highest Profitability)Moving Averages (Self-Adjusting Parameters for Highest Profitability)

It is a dual moving average crossover system - Smart Moving Averages .

Moving averages are used to identify current price developments and the potential for a change in an established trend.

The crossover in a dual moving average system can be used as a trigger to buy or to sell an asset, or as a trend reversal indication.

The crossover occurrence depends on the periods for which the moving averages are calculated. Using constant period values may not bring the best results.

The Smart Moving Averages change their periods automatically to get the highest profitability .

The concept is similar to the Smart SuperTrend .

Features:

• Self-Adjusting Period parameters

• The graphs for Profitability, Moving Average 1 Period, Moving Average 2 Period and the Moving Averages themselves are available to choose for display from the indicator settings

• A chart layout can be made just for the Smart Moving Averages, having all the graphs nicely displayed

• Alerts for changes in Trend, Moving Average 1 Period, Moving Average 2 Period, Profitability

• Different types of Moving Averages are available to choose from in the indicator settings (SMA, EMA, RMA, WMA, VWMA, DEMA, TEMA, HullMA, TMA).

The range for Moving Average 1 Period, Moving Average 2 Period and Time can be changed in the indicator settings (suggested optimal values are displayed on the chart).

This affects the loading speed (smaller range, faster to load), as well as the accuracy of the signals.

The indicator switches to the most profitable Moving Average 1 Period and Moving Average 2 Period parameters automatically, in real-time.

It scans across the entire historical data made available by TradingView.

The Smart Moving Average system works on all timeframes and symbols available on TradingView.

Exception for when the Volume Weighted Moving Average is used - it doesn't work for symbols without volume data.

It does not repaint!

But several aspects must be considered:

- 1. TradingView periodically removes access to old data while giving access to new data in real-time.

____ The frequency depends on the timeframe, amount of data. It can happen daily for second charts, weekly for minute charts.

____ Since the Indicator wouldn't have access to that old data anymore, the Profitability may change its value, causing a certain degree of repainting.

- 2. The starting time for Backtest must be inserted in the settings panel.

____ As long as the starting time has available price data, the Smart Moving Averages will NOT get repainted.

____ A suggested starting date for the analysis is shown on the chart. Insert the date in the indicator settings.

This indicator is compatible with the Wrapper Module of the Risk Management System indicator, which means they can work together as a trading bot.

스크립트에서 "moving average crossover"에 대해 찾기

APEX - Moving Averages [v1]A moving average is the most known indicator that takes into consideration price from the last several periods of the price and calculates a smoothed line also known as a Moving average. This way you will cut out a lot of the noise and have a different view.

The most common usage is the moving average crossover system when you buy and sell when a crossover happens. This system is in general not very profitable but can be used effectively in trending markets.

There is really no general rule to what length should be used. The most well-known and respected lengths are 20 / 50 / 100 / 200 for almost all average. These values are respected as strong resistance and support levels. but if you plan to use a crossover Systems the most profitable settings tend to be when the averages are close together 14 and 28 etc. But this is an area I would appeal to for you to really try out what works and what does not.

Other uses of moving averages are the following:

Crossover system

Moving averages are pointing up and price crosses below (Buy Pullback)

The slow-moving average is Below the fast moving average to help to identify possible bullishness

Can be used as support and resistance lines

If you are an advanced user you may want to try out the following techniques:

Create your own moving average by combining several of those together with the source function

Using the Average True Range to create Keltner Channels

Using Standard deviation to create Bollinger bands (Bollinger bands are also accessible on their own)

You can use Moving averages to smooth the noise on other indicators such as RSI / CCI / MFI

Granville 8-Rule Engine — v6Description:

The Granville 8-Rule Engine systematically implements Joseph Granville's eight original trading rules, which provide a comprehensive framework for interpreting price action relative to a moving average to identify genuine trend changes and avoid false signals.

Granville's methodology focuses on the critical relationship between price movement and the direction of the moving average, recognizing that valid trend changes and continuations exhibit specific behavioral patterns while false breakouts and reversals show characteristic divergences.

The indicator evaluates all eight of Granville's rules and assigns a composite score based on their fulfillment:

Bullish Rules:

Rule 1: Price crosses above a rising moving average (+3 points)

Rule 2: Price remains above a rising moving average after testing support (+2 points)

Rule 3: Price remains above a rising moving average after penetrating below it (+1 point)

Rule 4: Moving average changes from declining to rising (+1 point)

Bearish Rules:

Rule 5: Price crosses below a declining moving average (-3 points)

Rule 6: Price remains below a declining moving average after testing resistance (-2 points)

Rule 7: Price remains below a declining moving average after penetrating above it (-1 point)

The indicator incorporates volume confirmation by adding or subtracting additional points when significant volume accompanies the fulfillment of bullish or bearish rules, respectively.

A buy signal is generated when the composite score reaches +4 or higher, indicating multiple bullish rules are simultaneously satisfied. A sell signal is generated when the score reaches -4 or lower, indicating multiple bearish rules are in effect.

This systematic approach filters out many false breakout and whipsaw signals by requiring multiple confirmatory conditions rather than relying on simple moving average crossovers. The scoring mechanism provides a quantitative measure of the strength of the prevailing trend relationship, enabling traders to distinguish between genuine trend development and deceptive price movements that fail to confirm with the moving average direction.

The Granville 8-Rule Engine provides a disciplined, rule-based method for determining whether price movements represent valid trend continuation, genuine trend reversal, or potentially misleading counter-trend activity that is likely to fail. By requiring multiple confirmatory conditions from Granville's established rules, the indicator helps traders avoid premature entries and provides higher-probability signals for participating in sustained trend movements.

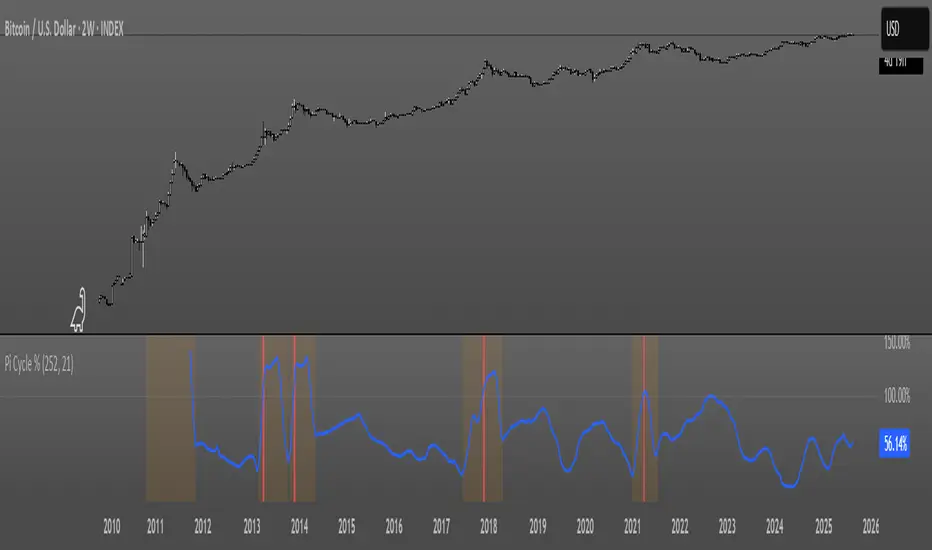

Pi Cycle OscillatorThis oscillator combines the Pi Cycle Top indicator with a percentile-based approach to create a more precise and easy to read market timing tool.

Instead of waiting for moving average crossovers, it shows you exactly how close you are to a potential market top.

Orange background means you should start preparing for a potential top and look into taking profits.

Red background means that the crossover has happened on the original Pi Cycle Indicator and that you should have already sold everything. (Crossover of the gray line aka 100)

Thank you

Bollinger Band Width Percentile - The_Caretaker

Pi Cycle Top - megasyl20

OB/OS adaptative v1.1# OB/OS Adaptative v1.1 - Multi-Timeframe Adaptive Overbought/Oversold Indicator

## Overview

The `tradingview_indicator_emas.pine` script is a sophisticated multi-timeframe indicator designed to identify dynamic overbought and oversold levels in financial markets. It combines EMA (Exponential Moving Average) crossovers and Bollinger Bands across monthly, weekly, and daily timeframes to create adaptive support and resistance levels that adjust to changing market conditions.

## Core Functionality

### Multi-Timeframe Analysis

The indicator analyzes three timeframes simultaneously:

- **Monthly (M)**: Long-term trend identification

- **Weekly (W)**: Intermediate-term trend identification

- **Daily (D)**: Short-term volatility measurement

### Technical Indicators Used

- **EMA 9 and EMA 20**: For trend identification and momentum assessment

- **Bollinger Bands (20-period)**: For volatility measurement and extreme level identification

- **Price action**: For confirmation of level validity and signal generation

## Key Features

### Adaptive Level Calculation

The indicator dynamically determines overbought and oversold levels based on market structure and trend bias:

#### Monthly Level Logic

- **Bullish Bias** (when monthly open > EMA20):

- Oversold = lower of EMA9 or EMA20

- Overbought = upper of EMA9 or Bollinger Upper Band

- **Bearish/Neutral Bias** (when monthly open ≤ EMA20):

- Oversold = Bollinger Lower Band

- Overbought = upper of EMA20 or EMA9

#### Weekly Level Logic

- **Bullish Bias** (when weekly open > EMA20):

- Oversold = lower of EMA9 or EMA20

- Overbought = Bollinger Upper Band

- **Bearish/Neutral Bias** (when weekly open ≤ EMA20):

- Oversold = Bollinger Lower Band

- Overbought = upper of EMA20 or EMA9

#### Daily Level Logic

- Simple Bollinger Bands:

- Oversold = Bollinger Lower Band

- Overbought = Bollinger Upper Band

### Final Level Determination

The indicator combines all three timeframes through a weighted averaging process:

1. Calculates initial values as the average of monthly, weekly, and daily levels

2. Ensures mathematical consistency by enforcing overbought_final ≥ oversold_final using min/max functions

3. Calculates a midpoint average level as the center of the range

### Visual Elements

- **Dynamic Lines**: Draws horizontal lines for current and previous period overbought, oversold, and average levels

- **Labels**: Places clear textual labels at the start of each period

- **Color Coding**:

- Red for overbought levels (resistance)

- Green for oversold levels (support)

- Blue for average levels (pivot point)

- **Transparency**: Previous period lines use semi-transparent colors to distinguish between current and historical levels

### Update Mechanism

- **Calculation Day**: User-defined day of the week (default: Monday)

- On the specified calculation day, the indicator:

- Updates all levels based on previous bar's data

- Draws new lines extending forward for a user-defined number of days

- Maintains previous period lines for comparison and trend analysis

- Automatically deletes and recreates lines to ensure clean visualization

### Proximity Detection

- Alerts when price approaches overbought/oversold levels (configurable distance in percentage)

- Helps identify potential reversal zones before actual crossovers occur

- Distance thresholds are user-configurable for both overbought and oversold conditions

### Alert Conditions

The indicator provides four distinct alert types:

1. **Cross below oversold**: Triggered when price crosses below the oversold level

2. **Cross above overbought**: Triggered when price crosses above the overbought level

3. **Near oversold**: Triggered when price approaches the oversold level within the configured distance

4. **Near overbought**: Triggered when price approaches the overbought level within the configured distance

### Debug Mode

When enabled, displays comprehensive debug information including:

- Current values for all levels (oversold, overbought, average)

- Timeframe-specific calculations and raw data points

- System status information (current day, calculation day, etc.)

- Lines existence and timing information

- Organized in multiple labels at different price levels to avoid overlap

## Configuration Parameters

| Parameter | Default Value | Description |

|---------|---------------|-------------|

| Short EMA (9) | 9 | Length for short-term EMA calculation |

| Long EMA (20) | 20 | Length for long-term EMA calculation |

| BB Length | 20 | Period for Bollinger Bands calculation |

| Std Dev | 2.0 | Standard deviation multiplier for Bollinger Bands |

| Distance to overbought (%) | 0.5 | Percentage threshold for "near overbought" alerts |

| Distance to oversold (%) | 0.5 | Percentage threshold for "near oversold" alerts |

| Calculation day | Monday | Day of week when levels are recalculated |

| Lookback days | 7 | Number of days to extend previous period lines backward |

| Forward days | 7 | Number of days to extend current period lines forward |

| Show Debug Labels | false | Toggle for comprehensive debug information display |

## Trading Applications

### Primary Use Cases

1. **Reversal Trading**: Identify potential reversal zones when price approaches overbought/oversold levels

2. **Trend Confirmation**: Use the adaptive nature of levels to confirm trend strength and direction

3. **Position Sizing**: Adjust position size based on distance from key levels

4. **Stop Placement**: Use opposite levels as dynamic stop-loss references

### Strategic Advantages

- **Adaptive Nature**: Levels adjust to changing market volatility and trend structure

- **Multi-Timeframe Confirmation**: Signals are validated across multiple timeframes

- **Visual Clarity**: Clear color-coded lines and labels enhance decision-making

- **Proactive Alerts**: "Near" conditions provide early warnings before crossovers

## Implementation Details

### Data Security

Uses `request.security()` function to fetch data from higher timeframes (monthly, weekly) while maintaining proper bar indexing with ` ` offset for open prices.

### Performance Optimization

- Uses `var` keyword to declare persistent variables that maintain state across bars

- Efficient line and label management with proper deletion before recreation

- Conditional execution of debug code to minimize performance impact

### Error Handling

- Comprehensive NA (not available) checks throughout the code

- Graceful degradation when data is unavailable for higher timeframes

- Mathematical safeguards to prevent invalid level calculations

## Conclusion

The OB/OS Adaptative v1.1 indicator represents a sophisticated approach to identifying market extremes by combining multiple technical analysis concepts. Its adaptive nature makes it particularly useful in trending markets where static levels may be less effective. The multi-timeframe approach provides a comprehensive view of market structure, while the visual elements and alert system enhance its practical utility for active traders.

MA Crossover [AlchimistOfCrypto]🌌 MA Crossover Quantum – Illuminating Market Harmonic Patterns 🌌

Category: Trend Analysis Indicators 📈

"The moving average crossover, reinterpreted through quantum field principles, visualizes the underlying resonance structures of price movements. This indicator employs principles from molecular orbital theory where energy states transition through gradient fields, similar to how price momentum shifts between bullish and bearish phases. Our implementation features algorithmically optimized parameters derived from extensive Python-based backtesting, creating a visual representation of market energy flows with dynamic opacity gradients that highlight the catalytic moments where trend transformations occur."

📊 Professional Trading Application

The MA Crossover Quantum transcends the traditional moving average crossover with a sophisticated gradient illumination system that highlights the energy transfer between fast and slow moving averages. Scientifically optimized for multiple timeframes and featuring eight distinct visual themes, it enables traders to perceive trend transitions with unprecedented clarity.

⚙️ Indicator Configuration

- Timeframe Presets 📏

Python-optimized parameters for specific timeframes:

- 1H: EMA 23/395 - Ideal for intraday precision trading

- 4H: SMA 41/263 - Balanced for swing trading operations

- 1D: SMA 8/44 - Optimized for daily trend identification

- 1W: SMA 32/38 - Calibrated for medium-term position trading

- 2W: SMA 17/20 - Engineered for long-term investment signals

- Custom Settings 🎯

Full parameter customization available for professional traders:

- Fast/Slow MA Length: Fine-tune to specific market conditions

- MA Type: Select between EMA (exponential) and SMA (simple) calculation methods

- Visual Theming 🎨

Eight scientifically designed visual palettes optimized for neural pattern recognition:

- Neon (default): High-contrast green/red scheme enhancing trend transition visibility

- Cyan-Magenta: Vibrant palette for maximum visual distinction

- Yellow-Purple: Complementary colors for enhanced pattern recognition

- Specialized themes (Green-Red, Forest Green, Blue Ocean, Orange-Red, Grayscale): Each calibrated for different market environments

- Opacity Control 🔍

- Variable transparency system (0-100) allowing seamless integration with price action

- Adaptive glow effect that intensifies around crossover points - the "catalytic moments" of trend change

🚀 How to Use

1. Select Timeframe ⏰: Choose from scientifically optimized presets based on your trading horizon

2. Customize Parameters 🎚️: For advanced users, disable presets to fine-tune MA settings

3. Choose Visual Theme 🌈: Select a color scheme that enhances your personal pattern recognition

4. Adjust Opacity 🔎: Fine-tune visualization intensity to complement your chart analysis

5. Identify Trend Changes ✅: Monitor gradient intensity to spot high-probability transition zones

6. Trade with Precision 🛡️: Use gradient intensity variations to determine position sizing and risk management

Developed through rigorous mathematical modeling and extensive backtesting, MA Crossover Quantum transforms the fundamental moving average crossover into a sophisticated visual analysis tool that reveals the molecular structure of market momentum.

Buy Signal Forex & Crypto v0 ImprovedPurpose of the Script:

This script is designed to generate buy and sell signals for trading Forex and cryptocurrencies by analyzing price trends using exponential moving averages (EMAs), volatility, and volume filters. The signals are displayed as arrows on the chart.

What the Script Does

Input Settings:

The script allows the user to configure various settings, such as the lengths of EMAs, a higher timeframe for trend confirmation, and thresholds for volume and volatility (ATR - Average True Range).

Key settings:

5 EMA Length – Length of the short-term EMA.

13 EMA Length – Length of the medium-term EMA.

26 EMA Length – Length of the long-term EMA.

21 EMA Length – Used for trend confirmation on a higher timeframe.

Higher Timeframe – Lets you select a timeframe (e.g., daily) for confirming the overall trend.

ATR Threshold – Filters out signals when the market's volatility is too low.

Volume Filter – Ensures sufficient trading activity before generating signals.

Calculating EMAs (Exponential Moving Averages):

Four EMAs are calculated:

ema5 (short-term), ema13 (medium-term), ema26 (long-term), and ema21 (higher timeframe confirmation).

These EMAs help determine price trends and crossovers, which are critical for identifying buy and sell opportunities.

Trend Confirmation Using a Higher Timeframe:

The 21 EMA on the higher timeframe (e.g., daily) is used to confirm the overall direction of the market.

Defining Signal Conditions:

Buy Signal:

A buy signal is generated when:

ema5 crosses above ema13 (indicating a bullish trend).

ema5 crosses above ema26 (stronger bullish confirmation).

The closing price is above ema5, ema13, ema26, and the 21 EMA on the higher timeframe.

The market's volatility (ATR) is above the defined threshold.

The volume meets the conditions or volume filtering is disabled.

Sell Signal:

A sell signal is generated when:

ema5 crosses below ema13 (indicating a bearish trend).

ema5 crosses below ema26 (stronger bearish confirmation).

The closing price is below ema5, ema13, ema26, and the 21 EMA on the higher timeframe.

The market's volatility (ATR) is above the defined threshold.

The volume meets the conditions or volume filtering is disabled.

Volume Filtering:

Ensures there’s enough trading activity by comparing the current volume to a 20-period moving average of volume.

Persistent Variables:

These variables (crossed13 and crossed13Sell) help track whether the short-term EMA (ema5) has crossed the medium-term EMA (ema13). This prevents false or repeated signals.

Displaying Signals on the Chart:

Buy signals are displayed as green upward arrows below the price.

Sell signals are displayed as red downward arrows above the price.

How It Helps Traders:

This script provides visual cues for potential entry and exit points by combining moving average crossovers, volatility, volume, and higher timeframe trend confirmation. It works well for trending markets and ensures signals are filtered for stronger conditions to reduce noise.

OBV Oscillator [LazyBear]- with some MAsThis indicator in modified OBV written by @LazyBear

I just added the 2 different Bollinger Bands and 2 different moving averages to the OBV version of LazyBear.

OBV line green -> OBV above zero

OBV line red -> OBV under zero

green background line -> OBV crossover 1st Moving Average

red background line -> OBV crossunder 1st Moving Average

blue '◆' -> OBV crossover 2nd Moving Average

yellow '◆' -> OBV crosunder 2nd Moving Average

blue '+' -> 1st Moving Average crossUNDER 2nd Moving Average

red '+' -> 1st Moving Average crossOVER 2nd Moving Average

MA Crossover Alerts for Small Quick Profits on 3commas/DCA botDear fellow 3commas users,

This is a the most basic Moving Average crossover technique generating Buy Alerts.

This is especially written for those of you who want to link this basic crossover strategy with your 3commas DCA bot .

Buy Alerts

Moving averages available:

- Simple Moving Average (SMA)

- Exponential Moving Average (EMA)

- Weighted Moving Average (WMA)

- Hull Moving Average (HullMA)

- Volume Weighted Moving Average (VMWA)

- Running Moving Average (RMA)

- Triple Exponential Moving Average (TEMA)

Recommended settings for using with 3commas DCA bot:

Interval:

3m to 15m

3commas bot setup:

- TP/TTP: 0.3%/0.1%,

- Base Order: Your choice ,

- Safety Order: 1.2 * Base order

- Safety Order Volume Scale: 1.2,

- Safety Order Step Scale: 1.5,

- Max Active Deals: Your choice ,

- Price Deviation to Open Safety Order (% from initial order): 0.2%,

- Max Safety Trades Count: 7,

- Simulatenous Deals per Same Pair: 3

> Create Alert with Buy Alert and link it to your bot "Message for deal start signal"

10 indicators in 1 : MACD RSI PIVOT EMA-CROSS and 7 EMA/SMA10 indicators in 1

MACD

RSI

PIVOT weekly:best

200 sma

100 sma

75 ema

55 ema

50 sma

20 ema

Golden EMA Crossover 13/48 based on tests Results of 1750 Moving Average Crossovers

Alert included, You can find "Bullish signal" and "Bearish signal" When you add Alert

Efmus System : 10 indicators in 1

10 indicators in 1

MACD

RSI

PIVOT weekly:best

200 sma

100 sma

75 ema

55 ema

50 sma

20 ema

Golden EMA Crossover 13/48 based on tests Results of 1750 Moving Average Crossovers :

etfhq.com

Efmus System : 10 indicators in 1

10 indicators in 1

MACD

RSI

PIVOT weekly:best

200 sma

100 sma

75 ema

55 ema

50 sma

20 ema

Golden EMA Crossover 13/48 based on tests Results of 1750 Moving Average Crossovers :

etfhq.com

Adaptive Trend SelectorThe Adaptive Trend Selector is a comprehensive trend-following tool designed to automatically identify the optimal moving average crossover strategy. It features adjustable parameters and an integrated backtester that delivers institutional-grade insights into the recommended strategy. The model continuously adapts to new data in real time by evaluating multiple moving average combinations, determining the best performing lengths, and presenting the backtest results in a clear, color-coded table that benchmarks performance against the buy-and-hold strategy.

At its core, the model systematically backtests a wide range of moving average combinations to identify the configuration that maximizes the selected optimization metric. Users can choose to optimize for absolute returns or risk-adjusted returns using the Sharpe, Sortino, or Calmar ratios. Alternatively, users can enable manual optimization to test custom fast and slow moving average lengths and view the corresponding backtest results. The label displays the Compounded Annual Growth Rate (CAGR) of the strategy, with the buy-and-hold CAGR in parentheses for comparison. The table presents the backtest results based on the fast and slow lengths displayed at the top:

Sharpe = CAGR per unit of standard deviation.

Sortino = CAGR per unit of downside deviation.

Calmar = CAGR relative to maximum drawdown.

Max DD = Largest peak-to-trough decline in value.

Beta (β) = Return sensitivity relative to buy-and-hold.

Alpha (α) = Excess annualized risk-adjusted returns.

Win Rate = Ratio of profitable trades to total trades.

Profit Factor = Total gross profit per unit of losses.

Expectancy = Average expected return per trade.

Trades/Year = Average number of trades per year.

This indicator is designed with flexibility in mind, enabling users to specify the start date of the backtesting period and the preferred moving average strategy. Supported strategies include the Exponential Moving Average (EMA), Simple Moving Average (SMA), Wilder’s Moving Average (RMA), Weighted Moving Average (WMA), and Volume-Weighted Moving Average (VWMA). To minimize overfitting, users can define constraints such as a minimum and maximum number of trades per year, as well as an optional optimization margin that prioritizes longer, more robust combinations by requiring shorter-length strategies to exceed this threshold. The table follows an intuitive color logic that enables quick performance comparison against buy-and-hold (B&H):

Sharpe = Green indicates better than B&H, while red indicates worse.

Sortino = Green indicates better than B&H, while red indicates worse.

Calmar = Green indicates better than B&H, while red indicates worse.

Max DD = Green indicates better than B&H, while red indicates worse.

Beta (β) = Green indicates better than B&H, while red indicates worse.

Alpha (α) = Green indicates above 0%, while red indicates below 0%.

Win Rate = Green indicates above 50%, while red indicates below 50%.

Profit Factor = Green indicates above 2, while red indicates below 1.

Expectancy = Green indicates above 0%, while red indicates below 0%.

In summary, the Adaptive Trend Selector is a powerful tool designed to help investors make data-driven decisions when selecting moving average crossover strategies. By optimizing for risk-adjusted returns, investors can confidently identify the best lengths using institutional-grade metrics. While results are based on the selected historical period, users should be mindful of potential overfitting, as past results may not persist under future market conditions. Since the model recalibrates to incorporate new data, the recommended lengths may evolve over time.

Han Algo - Moving average strategyHan Algo Indicator Strategy Description

Overview:

The Han Algo Indicator is designed to identify trend directions and signal potential buy and sell opportunities based on moving average crossovers. It aims to provide clear signals while filtering out noise and minimizing false signals.

Indicators Used:

Moving Averages:

200 SMA (Simple Moving Average): Used as a long-term trend indicator.

100 SMA: Provides a medium-term perspective on price movements.

50 SMA: Offers insights into shorter-term trends.

20 SMA: Provides a very short-term perspective on recent price actions.

Trend Identification:

The indicator identifies the trend based on the relationship between the closing price (close) and the 200 SMA (ma_long):

Uptrend: When the closing price is above the 200 SMA.

Downtrend: When the closing price is below the 200 SMA.

Sideways: When the closing price is equal to the 200 SMA.

Buy and Sell Signals:

Buy Signal: Generated when transitioning from a downtrend to an uptrend (buy_condition):

Displayed as a green "BUY" label above the price bar.

Sell Signal: Generated when transitioning from an uptrend to a downtrend (sell_condition):

Displayed as a red "SELL" label below the price bar.

Signal Filtering:

Signals are filtered to prevent consecutive signals occurring too closely (min_distance_bars parameter):

Ensures that only significant trend reversals are captured, minimizing false signals.

Visualization:

Background Color:

Changes to green for uptrend and red for downtrend (bgcolor function):

Provides visual cues for current market sentiment.

Usage:

Traders can customize the indicator's parameters (long_term_length, medium_term_length, short_term_length, very_short_term_length, min_distance_bars) to align with their trading preferences and timeframes.

The Han Algo Indicator helps traders make informed decisions by highlighting potential trend reversals and aligning with market trends identified through moving average analysis.

Disclaimer:

This indicator is intended for educational purposes and as a visual aid to support trading decisions. It should be used in conjunction with other technical analysis tools and risk management strategies.

Multiple MAs Signals with RSI MA Filter & Signal About the Script

The "Multiple Moving Averages Signals with RSI MA Filter and Golden Signals" script is a comprehensive trading tool designed to provide traders with detailed insights and actionable signals based on multiple moving averages and RSI (Relative Strength Index). This script combines traditional moving average crossovers with RSI filtering to enhance the accuracy of trading signals and includes "golden" signals to highlight significant long-term trend changes.

This script integrates several technical indicators and concepts to create a robust and versatile trading tool. Here's why this combination is both original and useful:

1. Multiple Moving Averages:

- Why Use Multiple MAs: Different types of moving averages (SMA, EMA, SMMA, WMA, VWMA, Hull) offer unique perspectives on price trends and volatility. Combining them allows traders to capture a more comprehensive view of the market.

- Purpose: Using multiple moving averages helps identify trend direction, support/resistance levels, and potential reversal points.

2. RSI MA Filter:

- Why Use RSI: RSI is a momentum oscillator that measures the speed and change of price movements. It is used to identify overbought or oversold conditions in a market.

- Purpose: Filtering signals with RSI moving averages ensures that trades are taken in line with the prevailing momentum, reducing the likelihood of false signals.

3. Golden Signals:

- Why Use Golden Crosses: A golden cross (50-period MA crossing above the 200-period MA) is a well-known bullish signal, while a death cross (50-period MA crossing below the 200-period MA) is bearish. These signals are widely followed by traders and institutions.

- Purpose: Highlighting these significant long-term signals helps traders identify major buy or sell opportunities and align with broader market trends.

How the Script Works

1. Moving Average Calculations:

- The script calculates multiple moving averages (MA1 to MA5) based on user-selected types (SMA, EMA, SMMA, WMA, VWMA, Hull) and periods (9, 21, 50, 100, 200).

- Golden Moving Averages: Separately calculates 50-period and 200-period moving averages for generating golden signals.

2. RSI and RSI MA Filter:

- RSI Calculation: Computes the RSI for the given period.

- RSI MA: Calculates a moving average of the RSI to smooth out the RSI values and reduce noise.

- RSI MA Filter: Traders can enable/disable RSI filtering and set custom thresholds to refine long and short signals based on RSI momentum.

3. Long & Short Signal Generation:

- Long Signal: Generated when the short-term moving average crosses above both the mid-term and long-term moving averages, and the RSI MA is below the specified threshold (if enabled).

- Short Signal: Generated when the short-term moving average crosses below both the mid-term and long-term moving averages, and the RSI MA is above the specified threshold (if enabled).

4. Golden Signals:

- Golden Long Signal: Triggered when the 50-period golden moving average crosses above the 200-period golden moving average.

- Golden Short Signal: Triggered when the 50-period golden moving average crosses below the 200-period golden moving average.

How to Use the Script

1. Customize Inputs:

- Moving Averages: Choose the type of moving averages and set the periods for up to five different moving averages.

- RSI Settings: Adjust the RSI period and its moving average period. Enable or disable RSI filtering and set custom thresholds for long and short signals.

- Signal Colors: Customize the colors for long, short, and golden signals.

- Enable/Disable Signals: Toggle the visibility of long, short, and golden signals.

2. Observe Plots and Signals:

- The script plots the selected moving averages on the chart.

- Long and short signals are marked with labels on the chart, with customizable colors for easy identification.

- Golden signals are highlighted with specific labels to indicate significant long-term trend changes.

3. Analyze and Trade:

- Use the generated signals as part of your trading strategy. The script provides visual cues to help you make informed decisions about entering or exiting trades based on multiple technical indicators.

Unique Features

1. Integration of Multiple Moving Averages: Combines various moving average types to provide a holistic view of market trends.

2. RSI MA Filtering: Enhances signal accuracy by incorporating RSI momentum, reducing the likelihood of false signals.

3. Golden Signals: Highlights significant long-term trend changes, aligning with broader market movements.

4. Customizability: Offers extensive customization options, allowing traders to tailor the script to their specific trading strategies and preferences.

feel free to comments.

AllTheUpsTheresAlwaysDowns "AllTheUpsTheresAlwaysDowns" ☆ATUTAD☆ // w%r + ma indicator designed for forex trading.

This indicator combines the Williams %R, moving averages, and session tracking.

Key Inputs:

Williams%Range Period: Adjusts the sensitivity of the Williams %R calculation.

Moving Average Period: Defines the period for the moving average used in the indicator.

Overbought and Oversold Thresholds: Sets the thresholds for identifying overbought and oversold conditions.

Features:

Williams %R Calculation: Calculates the Williams %R, a momentum oscillator that measures overbought and oversold levels.

Moving Averages: Plots two moving averages to capitalize on and visualize trend direction.

Session Tracking: Identifies the start and end of trading sessions (Tokyo, London, New York) for better session-based analysis.

Signal Generation: Generates buy/sell signals based on Williams %R levels and moving average crossovers.

Color Coding: Visualizes color-coded bars and shapes to highlight different market conditions and signal types.

Alerts: For buy/sell signals and overbought/oversold conditions to prompt timely actions.

Usage Tips:

Interpret Signals: Trend direction through buy/sell signals and overbought/oversold trend,- reversal / breakout line conditions for potential trading opportunities.

Session Awareness: Take into account the trading sessions (Tokyo, London, New York) to move along with the market dynamics during different times of the day.

Confirmation: Use additional technical analysis tools to confirm signals before executing trades. For example the Williams Percetange Range indicator.

Risk Management: Trade with proper risk management strategies to avoid potential losses.

HappyTrading

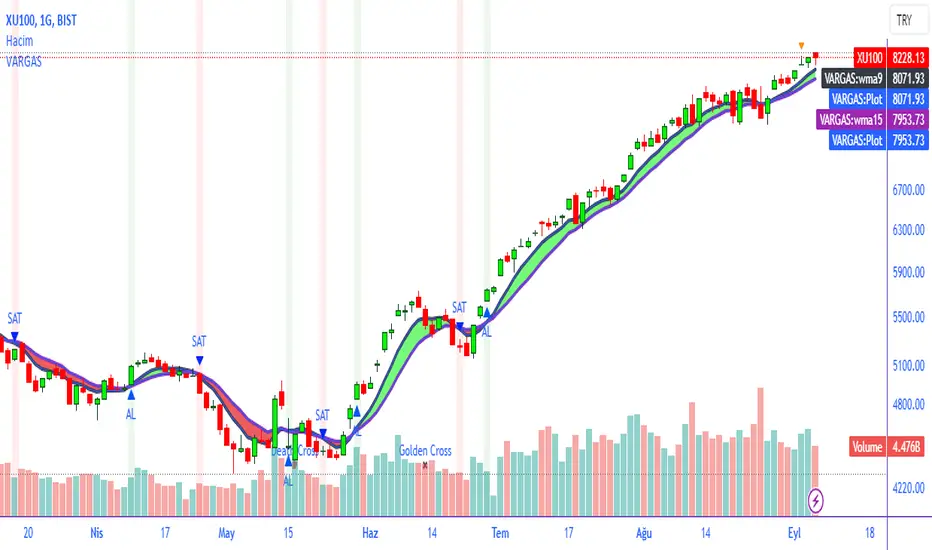

VARGAS"VARGAS" is an indicator that can be used in all timeframes on charts in the stock, crypto, and commodity markets. It allows trades to be opened according to the intersections of moving averages in different time periods.

It is an indicator using weighted moving averages. Using a weighted moving average has the following benefits for traders:

1) Precision and Smoothness: The WMA typically gives more weight to recent prices and therefore reacts faster to more recent data. This helps you catch price movements faster and recognize trend changes faster. On the other hand, the WMA is smoother than the simple moving average (SMA), which makes it less likely to generate false signals.

2) Trend Identification: The WMA is used to identify and analyze price trends. It is especially important for traders who want to track short-term movements. The WMA is used to assess the direction and strength of the trend.

3) Trading Signals: The WMA is used as part of various trading strategies. It is especially used in moving average crossover strategies. For example, a short-term WMA crossing the long-term WMA to the upside can be considered a buy signal, while a reversal can be interpreted as a sell signal.

4) Adaptability to Volatility: WMA can adapt to volatility by changing weighting factors. Investors can adopt a more flexible approach by assigning different weights based on market conditions and asset classes.

5) Data Correction: WMA can be helpful in reducing data noise. A single large price fluctuation can cause the SMA to be more affected, while the WMA reduces the impact of these fluctuations.

In our VARGAS coding, the intersection times of the 9-day and 15-day weighted moving averages allow us to decide the direction of the trend. The green and red cloud areas following the price candles make the strategy easy for the user to follow.

At the intersection between the 9-day weighted moving average and the 15-day weighted moving average, we can use buy and sell signals as follows:

If the 9-day weighted moving average crosses the 15-day weighted moving average upwards, buy,

Sell if the 9-day weighted moving average crosses the 15-day weighted moving average downwards.

Within the scope of this strategy, GOLDEN CROSS and DEATH CROSS intersections, which guide us for trend changes, are also included in the coding. Thus, it is aimed to add strength to our WMA 9 and WMA 15 intersection strategy as an idea.

VARGAS indicator gives better results for longer periods of 4 hours and above. As the time period increases, the probability of correct results will increase.

**

"VARGAS" hisse senedi, kripto, ve emtia piyasalarındaki grafiklerde her türlü zaman diliminde kullanılabilen bir indikatördür. Farklı zaman periyotlarındaki hareketli ortalamaların kesişimlerine göre işlem açılmasını sağlar.

Ağırlıklı hareketli ortalamalar kullanılarak hazırlanmış bir göstergedir. Ağırlıklı hareketli ortalama kullanmanın yatırımcılara aşağıdaki gibi faydaları bulunmaktadır:

1) Duyarlılık ve Pürüzsüzlük: WMA, tipik olarak son dönem fiyatlarına daha fazla ağırlık verir ve bu nedenle daha güncel verilere daha hızlı tepki verir. Bu, fiyat hareketlerini daha hızlı yakalamanıza ve daha hızlı trend değişikliklerini tanımanıza yardımcı olur. Diğer yandan, WMA, basit hareketli ortalamaya (SMA) göre daha pürüzsüzdür, bu da yanlış sinyal üretme olasılığını azaltır.

2) Trend Belirleme: WMA, fiyat trendlerini belirlemek ve analiz etmek için kullanılır. Özellikle kısa vadeli hareketleri izlemek isteyen yatırımcılar için önemlidir. WMA, trendin yönünü ve gücünü değerlendirmek için kullanılır.

3) Ticaret Sinyalleri: WMA, çeşitli ticaret stratejilerinin bir parçası olarak kullanılır. Özellikle hareketli ortalama crossover stratejilerinde kullanılır. Örneğin, kısa vadeli WMA'nın uzun vadeli WMA'yı yukarı yönlü kesmesi bir alım sinyali olarak kabul edilebilir, tersine dönmesi ise bir satış sinyali olarak yorumlanabilir.

4) Volatiliteye Uyarlanabilirlik: WMA, ağırlıklandırma faktörlerini değiştirerek volatiliteye uyum sağlayabilir. Yatırımcılar, piyasa koşullarına ve varlık sınıflarına göre farklı ağırlıklar atayarak daha esnek bir yaklaşım benimseyebilirler.

5) Veri Düzeltme: WMA, veri gürültüsünü azaltmada yardımcı olabilir. Tek bir büyük fiyat dalgalanması, SMA'nın daha fazla etkilenmesine neden olabilirken, WMA bu dalgalanmaların etkisini azaltır.

VARGAS isimli kodlamamızda ise 9 günlük ve 15 günlük ağırlıklı hareketli ortalamaların kesişme zamanları trendin yönüne karar vermemizi sağlar. Fiyat mumlarını takip eden yeşil ve kırmızı bulut alanları stratejinin kullanıcı tarafından kolaylıkla takip edilmesini sağlamaktadır.

9 Günlük Ağırlıklı hareketli ortalama, 15 Günlük Ağırlıklı hareketli ortalama arasındaki kesişimde al ve sat sinyallerini şu şekilde kullanabiliriz:

Eğer 9 günlük ağırlıklı hareketli ortalama 15 günlük ağırlıklı hareketli ortalamayı yukarı doğru kesiyorsa al,

Eğer 9 günlük ağırlıklı hareketli ortalama, 15 günlük ağırlıklı hareketli ortalamayı aşağı doğru keserse sat.

Bu strateji kapsamında trend değişimleri için bizlere yön veren GOLDEN CROSS ve DEATH CROSS kesişimleri de kodlamanın içerisinde dahil edilmiştir. Böylelikle WMA 9 ve WMA 15 kesişim stratejimize fikir olarak güç katması hedeflenmiştir.

VARGAS indikatörü 4 saat ve üzeri daha uzun periyotlarda daha iyi sonuçlar vermektedir. Zaman periyodu büyüdükçe doğru sonuç verme olasılığı artacaktır.

Extreme Trend Reversal Points [HeWhoMustNotBeNamed]Using moving average crossover for identifying the change in trend is very common. However, this method can give lots of false signals during the ranging markets. In this algorithm, we try to find the extreme trend by looking at fully aligned multi-level moving averages and only look at moving average crossover when market is in the extreme trend - either bullish or bearish. These points can mean long term downtrend or can also cause a small pullback before trend continuation. In this discussion, we will also check how to handle different scenarios.

🎲 Components

🎯 Recursive Multi Level Moving Averages

Multi level moving average here refers to applying moving average on top of base moving average on multiple levels. For example,

Level 1 SMA = SMA(source, length)

Level 2 SMA = SMA(Level 1 SMA, length)

Level 3 SMA = SMA(Level 2 SMA, length)

..

..

..

Level n SMA = SMA(Level (n-1) SMA, length)

In this script, user can select how many levels of moving averages need to be calculated. This is achieved through " recursive moving average " algorithm. Requirement for building such algorithm was initially raised by @loxx

While I was able to develop them in minimal code with the help of some of the existing libraries built on arrays and matrix , I also thought why not extend this to find something interesting.

Note that since we are using variable levels - we will not be able to plot all the levels of moving average. (This is because plotting cannot be done in the loop). Hence, we are using lines to display the latest moving average levels in front of the last candle. Lines are color coded in such a way that least numbered levels are greener and higher levels are redder.

🎯 Finding the trend and range

Strength of fully aligned moving average is calculated based on position of each level with respect to other levels.

For example, in a complete uptrend, we can find

source > L(1)MA > L(2)MA > L(3)MA ...... > L(n-1)MA > L(n)MA

Similarly in a complete downtrend, we can find

source < L(1)MA < L(2)MA < L(3)MA ...... < L(n-1)MA < L(n)MA

Hence, the strength of trend here is calculated based on relative positions of each levels. Due to this, value of strength can range from 0 to Level*(Level-1)/2

0 represents the complete downtrend

Level*(Level-1)/2 represents the complete uptrend.

Range and Extreme Range are calculated based on the percentile from median. The brackets are defined as per input parameters - Range Percentile and Extreme Range Percentile by using Percentile History as reference length.

Moving average plot is color coded to display the trend strength.

Green - Extreme Bullish

Lime - Bullish

Silver - range

Orange - Bearish

Red - Extreme Bearish

🎯 Finding the trend reversal

Possible trend reversals are when price crosses the moving average while in complete trend with all the moving averages fully aligned. Triangle marks are placed in such locations which can help observe the probable trend reversal points. But, there are possibilities of trend overriding these levels. An example of such thing, we can see here:

In order to overcome this problem, we can employ few techniques.

1. After the signal, wait for trend reversal (moving average plot color to turn silver) before placing your order.

2. Place stop orders on immediate pivot levels or support resistance points instead of opening market order. This way, we can also place an order in the direction of trend. Whichever side the price breaks out, will be the direction to trade.

3. Look for other confirmations such as extremely bullish and bearish candles before placing the orders.

🎯 An example of using stop orders

Let us take this scenario where there is a signal on possible reversal from complete uptrend.

Create a box joining high and low pivots at reasonable distance. You can also chose to add 1 ATR additional distance from pivots.

Use the top of the box as stop-entry for long and bottom as stop-entry for short. The other ends of the box can become stop-losses for each side.

After few bars, we can see that few more signals are plotted but, the price is still within the box. There are some candles which touched the top of the box. But, the candlestick patterns did not represent bullishness on those instances. If you have placed stop orders, these orders would have already filled in. In that case, just wait for position to hit either stop or target.

For bullish side, targets can be placed at certain risk reward levels. In this case, we just use 1:1 for bullish (trend side) and 1:1.5 for bearish side (reversal side)

In this case, price hit the target without any issue:

Wait for next reversal signal to appear before placing another order :)

Signal Moving Average [LuxAlgo]The following script returns a moving average designed to be used as a signal line in a moving average crossover system. The moving average will diverge from the price during ranging markets and reach the value of a regular moving average during trending markets.

Settings

Length: Moving average period

Src: Source input of the indicator

Usage

Moving average crossover strategies often rely on a "signal" line, a slower moving average used to determine a general trend. This signal line is paired with a faster moving average to filter out potential whipsaw trades that would have been given from crosses between the regular price and the signal line.

The proposed indicator will avoid crossing the price by diverging from it during more ranging periods, thus effectively reducing the number of crosses produced between the price and the signal line.

The color of the area between the price and the signal line is determined by the position of the price relative to the signal line, with a green color indicator a price superior to the signal line.

The color of the signal line, however, is taking into account whether market is trending or ranging, only changing once the market is trending.

The chart above shows the cumulated number of crosses between the price and the signal line (green) and a regular simple moving average of the same period (red) on AMD 15m, a lowered number of crosses can effectively reduce the impact of frictional costs introduced by whipsaw trades.

trend_vol_stopThe description below is copied from the script's comments. Because TradingView does not allow me to edit this description, please refer to the script's comments section, as well as the release notes, for the most up-to-date information.

----------

Usage:

The inputs define the trend and the volatility stop.

Trend:

The trend is defined by a moving average crossover. When the short

(or fast) moving average is above the long (slow) moving average, the

trend is up. Otherwise, the trend is down. The inputs are:

long: the number of periods in the long/slow moving average.

short: the number of periods in the short/fast moving average.

The slow moving average is shown in various colors (see explanation

below. The fast moving average is a faint blue.

Volatility stop:

The volatility stop has two modes, percentage and rank. The percentage

stop is given in terms of annualized volatility. The rank stop is given

in terms of percentile.

stop_pct and stop_rank are initialized with "-1". You need to set one of

these to the values you want after adding the indicator to your chart.

This is the only setting that requires your input.

mode: choose "rank" for a rank stop, "percentage" for a percentage stop.

vol_window: the number of periods in the historical volatility

calculation. e.g. "30" means the volatility will be a weighted

average of the previous 30 periods. applies to both types of stop.

stop_pct: the volatility limit, annualized. for example, "50" means

that the trend will not be followed when historical volatility rises

above 50%.

stop_rank: the trend will not be followed when the volatility is in the

N-th percentile. for example, "75" means the trend will not be

followed when the current historical volatility is greater than 75%

of previous volatilities.

rank_window: the number of periods in the rank percentile calculation.

for example, if rank_window is "252" and "stop_rank" is "80", the

trend will not be followed when current historical volatility is

greater than 80% of the previous 252 historical volatilities.

Outputs:

The outputs include moving averages, to visually identify the trend,

a volatility table, and a performance table.

Moving averages:

The slow moving average is colored green in an uptrend, red in a

downtrend, and black when the volatility stop is in place.

Volatility table:

The volatility table gives the current historical volatility, annualized

and expressed as a whole number percentage. E.g. "65" means the

instrument's one standard deviation annual move is 65% of its price.

The current rank is expressed, also as a whole number percentage. E.g.

"15" means the current volatility is greater than 15% of previous

volatilities. For convenience, the volatilities corresponding to the

0, 25, 50, 75, and 100th percentiles are also shown.

Performance table:

The performance table shows the current strategy's performance versus

buy-and-hold. If the trend is up, the instrument's return for that

period is added to the strategy's return, because the strategy is long.

If the trend is down, the negative return is added, because the strategy

is short. If the volatility stop is in (the slow moving average is

black), that period's return is excluded from the strategy returns.

Every period's return is added to the buy-and-hold returns.

The table shows the average return, the standard deviation of returns,

and the sharpe ratio (average return / standard deviation of returns).

All figures are expressed as per-period, whole number percentages.

For exmaple, "0.1" in the mean column on a daily chart means a

0.1% daily return.

The number of periods (samples) for each strategy is also shown.

Consensio Trading SystemConsensio Trading System involves using 3 different moving average comprised of 2, 7 and 30-week simple moving average. The trading methodology is simple when all moving average are above one another and is converging up ..You're in a bull market and vise versa for a bear market when all the moving average below one another and is converging down. There are said to be more than 1000 (1k) combination for this system to begin trade with and all pattern require at least 3 moving average. This system is mainly used with the weekly chart for longterm perspective although it can be used up to 30 min for short-term trade setups. The main component of this system is longer-term moving average i.e.30 period if that is down and other MA are consolidating within a range aka death cross back and forth ... the overall market should be considered bear market regardless of other two moving average crossovers.

Hyperwave Channel by Lucid Investment Strategies

Co-hosted by D. Tyler Jenks and Leah Wald

D. Tyler Jenks, the President, and CIO of Lucid Investment Strategies LLC developed the proprietary technical system of Hyperwave. After 40 years as an investment manager, he discovered over 300 examples of Hyperwaves within various asset classes; stocks, bonds, commodities , indexes, and cryptocurrencies

Impulse Reactor RSI-SMA Trend Indicator [ApexLegion]Impulse Reactor RSI-SMA Trend Indicator

Introduction and Theoretical Background

Design Rationale

Standard indicators frequently generate binary 'BUY' or 'SELL' signals without accounting for the broader market context. This often results in erratic "Flip-Flop" behavior, where signals are triggered indiscriminately regardless of the prevailing volatility regime.

Impulse Reactor was engineered to address this limitation by unifying two critical requirements: Quantitative Rigor and Execution Flexibility.

The Solution

Composite Analytical Framework This script is not a simple visual overlay of existing indicators. It is an algorithmic synthesis designed to function as a unified decision-making engine. The primary objective was to implement rigorous quantitative analysis (Volatility Normalization, Structural Filtering) directly within an alert-enabled framework. This architecture is designed to process signals through strict, multi-factor validation protocols before generating real-time notifications, allowing users to focus on structurally validated setups without manual monitoring.

How It Works

This is not a simple visual mashup. It utilizes a cross-validation algorithm where the Trend Structure acts as a gatekeeper for Momentum signals:

Logic over Lag: Unlike simple moving average crossovers, this script uses a 15-layer Gradient Ribbon to detect "Laminar Flow." If the ribbon is knotted (Compression), the system mathematically suppresses all signals.

Volatility Normalization: The core calculation adapts to ATR (Average True Range). This means the indicator automatically expands in volatile markets and contracts in quiet ones, maintaining accuracy without constant manual tweaking.

Adaptive Signal Thresholding: It incorporates an 'Anti-Greed' algorithm (Dynamic Thresholding) that automatically adjusts entry criteria based on trend duration. This logic aims to mitigate the risk of entering positions during periods of statistical trend exhaustion.

Why Use It?

Market State Decoding: The gradient Ribbon visualizes the underlying trend phase in real-time.

◦ Cyan/Blue Flow: Strong Bullish Trend (Laminar Flow).

◦ Magenta/Pink Flow: Strong Bearish Trend.

◦ Compressed/Knotted: When the ribbon lines are tightly squeezed or overlapping, it signals Consolidation. The system filters signals here to avoid chop.

Noise Reduction: The goal is not to catch every pivot, but to isolate high-confidence setups. The logic explicitly filters out minor fluctuations to help maintain position alignment with the broader trend.

⚖️ Chapter 1: System Architecture

Introduction: Composite Analytical Framework

System Overview

Impulse Reactor serves as a comprehensive technical analysis engine designed to synthesize three distinct market dimensions—Momentum, Volatility, and Trend Structure—into a unified decision-making framework. Unlike traditional methods that analyze these metrics in isolation, this system functions as a central processing unit that integrates disparate data streams to construct a coherent model of market behavior.

Operational Objective

The primary objective is to transition from single-dimensional signal generation to a multi-factor assessment model. By fusing data from the Impulse Core (Volatility), Gradient Oscillator (Momentum), and Structural Baseline (Trend), the system aims to filter out stochastic noise and identify high-probability trade setups grounded in quantitative confluence.

Market Microstructure Analysis: Limitations of Conventional Models

Extensive backtesting and quantitative analysis have identified three critical inefficiencies in standard oscillator-based strategies:

• Bounded Oscillator Limitations (The "Oscillation Trap"): Traditional indicators such as RSI or Stochastics are mathematically constrained between fixed values (0 to 100). In strong trending environments, these metrics often saturate in "overbought" or "oversold" zones. Consequently, traders relying on static thresholds frequently exit structurally valid positions prematurely or initiate counter-trend trades against prevailing momentum, resulting in suboptimal performance.

• Quantitative Blindness to Quality: Standard moving averages and trend indicators often fail to distinguish the qualitative nature of price movement. They treat low-volume drift and high-velocity expansion identically. This inability to account for "Volatility Quality" leads to delayed responsiveness during critical market events.

• Fractal Dissonance (Timeframe Disconnect): Financial markets exhibit fractal characteristics where trends on lower timeframes may contradict higher timeframe structures. Manual integration of multi-timeframe analysis increases cognitive load and susceptibility to human error, often resulting in conflicting biases at the point of execution.

Core Design Principles

To mitigate the aforementioned systemic inefficiencies, Impulse Reactor employs a modular architecture governed by three foundational principles:

Principle A:

Volatility Precursor Analysis Market mechanics demonstrate that volatility expansion often functions as a leading indicator for directional price movement. The system is engineered to detect "Volatility Deviation" — specifically, the divergence between short-term and long-term volatility baselines—prior to its manifestation in price action. This allows for entry timing aligned with the expansion phase of market volatility.

Principle B:

Momentum Density Visualization The system replaces singular momentum lines with a "Momentum Density" model utilizing a 15-layer Simple Moving Average (SMA) Ribbon.

• Concept: This visualization represents the aggregate strength and consistency of the trend.

• Application: A fully aligned and expanded ribbon indicates a robust trend structure ("Laminar Flow") capable of withstanding minor counter-trend noise, whereas a compressed ribbon signals consolidation or structural weakness.

Principle C:

Adaptive Confluence Protocols Signal validity is strictly governed by a multi-dimensional confluence logic. The system suppresses signal generation unless there is synchronized confirmation across all three analytical vectors:

1. Volatility: Confirmed expansion via the Impulse Core.

2. Momentum: Directional alignment via the Hybrid Oscillator.

3. Structure: Trend validation via the Baseline. This strict filtering mechanism significantly reduces false positives in non-trending (choppy) environments while maintaining sensitivity to genuine breakouts.

🔍 Chapter 2: Core Modules & Algorithmic Logic

Module A: Impulse Core (Normalized Volatility Deviation)

Operational Logic The Impulse Core functions as a volatility-normalized momentum gauge rather than a standard oscillator. It is designed to identify "Volatility Contraction" (Squeeze) and "Volatility Expansion" phases by quantifying the divergence between short-term and long-term volatility states.

Volatility Z-Score Normalization

The formula implements a custom normalization algorithm. Unlike standard oscillators that rely on absolute price changes, this logic calculates the Z-Score of the Volatility Spread.

◦ Numerator: (atr_f - atr_s) captures the raw momentum of volatility expansion.

◦ Denominator: (std_f + 1e-6) standardizes this value against historical variance.

◦ Result: This allows the indicator scales consistently across assets (e.g., Bitcoin vs. Euro) without manual recalibration.

f_impulse() =>

atr_f = ta.atr(fastLen) // Fast Volatility Baseline

atr_s = ta.atr(slowLen) // Slow Volatility Baseline

std_f = ta.stdev(atr_f, devLen) // Volatility Standard Deviation

(atr_f - atr_s) / (std_f + 1e-6) // Normalized Differential Calculation

Algorithmic Framework

• Differential Calculation: The system computes the spread between a Fast Volatility Baseline (ATR-10) and a Slow Volatility Baseline (ATR-30).

• Normalization Protocol: To standardize consistency across diverse asset classes (e.g., Forex vs. Crypto), the raw differential is divided by the standard deviation of the volatility itself over a 30-period lookback.

• Signal Generation:

◦ Contraction (Squeeze): When the Fast ATR compresses below the Slow ATR, it registers a potential volatility buildup phase.

◦ Expansion (Release): A rapid divergence of the Fast ATR above the Slow ATR signals a confirmed volatility expansion, validating the strength of the move.

Module B: Gradient Oscillator (RSI-SMA Hybrid)

Design Rationale To mitigate the "noise" and "false reversal" signals common in single-line oscillators (like standard RSI), this module utilizes a 15-Layer Gradient Ribbon to visualize momentum density and persistence.

Technical Architecture

• Ribbon Array: The system generates 15 sequential Simple Moving Averages (SMA) applied to a volatility-adjusted RSI source. The length of each layer increases incrementally.

• State Analysis:

Momentum Alignment (Laminar Flow): When all 15 layers are expanded and parallel, it indicates a robust trend where buying/selling pressure is distributed evenly across multiple timeframes. This state helps filter out premature "overbought/oversold" signals.

• Consolidation (Compression): When the distance between the fastest layer (Layer 1) and the slowest layer (Layer 15) approaches zero or the layers intersect, the system identifies a "Non-Tradable Zone," preventing entries during choppy market conditions.

// Laminar Flow Validation

f_validate_trend() =>

// Calculate spread between Ribbon layers

ribbon_spread = ta.stdev(ribbon_array, 15)

// Only allow signals if Ribbon is expanded (Laminar Flow)

is_flowing = ribbon_spread > min_expansion_threshold

// If compressed (Knotted), force signal to false

is_flowing ? signal : na

Module C: Adaptive Signal Filtering (Behavioral Bias Mitigation)

This subsystem, operating as an algorithmic "Anti-Greed" Mechanism, addresses the statistical tendency for signal degradation following prolonged trends.

Dynamic Threshold Adjustment

• Win Streak Detection: The algorithm internally tracks the outcome of closed trade cycles.

• Sensitivity Multiplier: Upon detecting consecutive successful signals in the same direction, a Penalty_Factor is applied to the entry logic.

• Operational Impact: This effectively raises the Required_Slope threshold for subsequent signals. For example, after three consecutive bullish signals, the system requires a 30% steeper trend angle to validate a fourth entry. This enforces stricter discipline during extended trends to reduce the probability of entering at the point of trend exhaustion.

Anti-Greed Logic: Dynamic Threshold Calculation

f_adjust_threshold(base_slope, win_streak) =>

// Adds a 10% penalty to the difficulty for every consecutive win

penalty_factor = 0.10

risk_scaler = 1 + (win_streak * penalty_factor)

// Returns the new, harder-to-reach threshold

base_slope * risk_scaler

Module D: Trend Baseline (Triple-Smoothed Structure)

The Trend Baseline serves as the structural filter for all signals. It employs a Triple-Smoothed Hybrid Algorithm designed to balance lag reduction with noise filtration.

Smoothing Stages

1. Volatility Banding: Utilizes a SuperTrend-based calculation to establish the upper and lower boundaries of price action.

2. Weighted Filter: Applies a Weighted Moving Average (WMA) to prioritize recent price data.

3. Exponential Smoothing: A final Exponential Moving Average (EMA) pass is applied to create a seamless baseline curve.

Functionality

This "Heavy" baseline resists minor intraday volatility spikes while remaining responsive to sustained structural shifts. A signal is only considered valid if the price action maintains structural integrity relative to this baseline

🚦 Chapter 3: Risk Management & Exit Protocols

Quantitative Risk Management (TP/SL & Trailing)

Foundational Architecture: Volatility-Adjusted Geometry Unlike strategies relying on static nominal values, Impulse Reactor establishes dynamic risk boundaries derived from quantitative volatility metrics. This design aligns trade invalidation levels mathematically with the current market regime.

• ATR-Based Dynamic Bracketing:

The protocol calculates Stop-Loss and Take-Profit levels by applying Fibonacci coefficients (Default: 0.786 for SL / 1.618 for TP) to the Average True Range (ATR).

◦ High Volatility Environments: The risk bands automatically expand to accommodate wider variance, preventing premature exits caused by standard market noise.

◦ Low Volatility Environments: The bands contract to tighten risk parameters, thereby dynamically adjusting the Risk-to-Reward (R:R) geometry.

• Close-Validation Protocol ("Soft Stop"):

Institutional algorithms frequently execute liquidity sweeps—driving prices briefly below key support levels to accumulate inventory.

◦ Mechanism: When the "Soft Stop" feature is enabled, the system filters out intraday volatility spikes. The stop-loss is conditional; execution is triggered only if the candle closes beyond the invalidation threshold.

◦ Strategic Advantage: This logic distinguishes between momentary price wicks and genuine structural breakdowns, preserving positions during transient volatility.

• Step-Function Trailing Mechanism:

To protect unrealized PnL while allowing for normal price breathing, a two-phase trailing methodology is employed:

◦ Phase 1 (Activation): The trailing function remains dormant until the price advances by a pre-defined percentage threshold.

◦ Phase 2 (Dynamic Floor): Once armed, the stop level creates a moving floor, adjusting relative to price action while maintaining a volatility-based (ATR) buffer to systematically protect unrealized PnL.

• Algorithmic Exit Protocols (Dynamic Liquidity Analysis)

◦ Rationale: Inefficiencies of Static Targets Static "Take Profit" levels often result in suboptimal exits. They compel traders to close positions based on arbitrary figures rather than evolving market structure, potentially capping upside during significant trends or retaining positions while the underlying trend structure deteriorates.

◦ Solution: Structural Integrity Assessment The system utilizes a Dynamic Liquidity Engine to continuously audit the validity of the position. Instead of targeting a specific price point, the algorithm evaluates whether the trend remains statistically robust.

Multi-Factor Exit Logic (The Tri-Vector System)

The Smart Exit protocol executes only when specific algorithmic invalidation criteria are met:

• 1. Momentum Exhaustion (Confluence Decay): The system monitors a 168-hour rolling average of the Confluence Score. A significant deviation below this historical baseline indicates momentum exhaustion, signaling that the driving force behind the trend has dissipated prior to a price reversal. This enables preemptive exits before a potential drawdown.

• 2. Statistical Over-Extension (Mean Reversion): Utilizing the core volatility logic, the system identifies instances where price deviates beyond 2.0 standard deviations from the mean. While the trend may be technically bullish, this statistical anomaly suggests a high probability of mean reversion (elastic snap-back), triggering a defensive exit to capitalize on peak valuation.

• 3. Oscillator Rejection (Immediate Pivot): To manage sudden V-shaped volatility, the system monitors RSI pivots. If a sharp "Pivot High" or divergence is detected, the protocol triggers an immediate "Peak Exit," bypassing standard trend filters to secure liquidity during high-velocity reversals.

🎨 Chapter 4: Visualization Guide

Gradient Oscillator Ribbon

The 15-layer SMA ribbon visualized via plot(r1...r15) represents the "Momentum Density" of the market.

• Visuals:

◦ Cyan/Blue Ribbon: Indicates Bullish Momentum.

◦ Pink/Magenta Ribbon: Indicates Bearish Momentum.

• Interpretation:

◦ Laminar Flow: When the ribbon expands widely and flows in parallel, it signifies a robust trend where momentum is distributed evenly across timeframes. This is the ideal state for trend-following.

◦ Compression (Consolidation): If the ribbon becomes narrow, twisted, or knotted, it indicates a "Non-Tradable Zone" where the market lacks a unified direction. Traders are advised to wait for clarity.

◦ Over-Extension: If the top layer crosses the Overbought (85) or Oversold (15) lines, it visually warns of potential market overheating.

Trend Baseline

The thick, color-changing line plotted via plot(baseline) represents the Structural Backbone of the market.

• Visuals: Changes color based on the trend direction (Blue for Bullish, Pink for Bearish).

• Interpretation:

Structural Filter: Long positions are statistically favored only when price action sustains above this baseline, while short positions are favored below it.

Dynamic Support/Resistance: The baseline acts as a dynamic support level during uptrends and resistance during downtrends.

Entry Signals & Labels

Text labels ("Long Entry", "Short Entry") appear when the system detects high-probability setups grounded in quantitative confluence.

• Visuals: Labeled signals appear above/below specific candles.

• Interpretation:

These signals represent moments where Volatility (Expansion), Momentum (Alignment), and Structure (Trend) are synchronized.

Smart Exit: Labels such as "Smart Exit" or "Peak Exit" appear when the system detects momentum exhaustion or structural decay, prompting a defensive exit to preserve capital.

Dynamic TP/SL Boxes

The semi-transparent colored zones drawn via fill() represent the risk management geometry.

• Visuals: Colored boxes extending from the entry point to the Take Profit (TP) and Stop Loss (SL) levels.

• Function:

Volatility-Adjusted Geometry: Unlike static price targets, these boxes expand during high volatility (to prevent wicks from stopping you out) and contract during low volatility (to optimize Risk-to-Reward ratios).

SAR + MACD Glow

Small glowing shapes appearing above or below candles.

• Visuals: Triangle or circle glows near the price bars.

• Interpretation:

This visual indicates a secondary confirmation where Parabolic SAR and MACD align with the main trend direction. It serves as an additional confluence factor to increase confidence in the trade setup.

Support/Resistance Table

A small table located at the bottom-right of the chart.

• Function: Automatically identifies and displays recent Pivot Highs (Resistance) and Pivot Lows (Support).

• Interpretation: These levels can be used as potential targets for Take Profit or invalidation points for manual Stop Loss adjustments.

🖥️ Chapter 5: Dashboard & Operational Guide

Integrated Analytics Panel (Dashboard Overview)

To facilitate rapid decision-making without manual calculation, the system aggregates critical market dimensions into a unified "Heads-Up Display" (HUD). This panel monitors real-time metrics across multiple timeframes and analytical vectors.

A. Intermediate Structure (12H Trend)

• Function: Anchors the intraday analysis to the broader market structure using a 12-hour rolling window.

• Interpretation:

◦ Bullish (> +0.5%): Indicates a positive structural bias. Long setups align with the macro flow.

◦ Bearish (< -0.5%): Indicates structural weakness. Short setups are statistically favored.

◦ Neutral: Represents a ranging environment where the Confluence Score becomes the primary weighting factor.

B. Composite Confluence Score (Signal Confidence)

• Definition: A probability metric derived from the synchronization of Volatility (Impulse Core), Momentum (Ribbon), and Trend (Baseline).

• Grading Scale:

Strong Buy/Sell (> 7.0 / < 3.0): Indicates full alignment across all three vectors. Represents a "Prime Setup" eligible for standard position sizing.

Buy/Sell (5.0–7.0 / 3.0–5.0): Indicates a valid trend but with moderate volatility confirmation.

Neutral: Signals conflicting data (e.g., Bullish Momentum vs. Bearish Structure). Trading is not recommended ("No-Trade Zone").

C. Statistical Deviation Status (Mean Reversion)

• Logic: Utilizes Bollinger Band deviation principles to quantify how far price has stretched from the statistical mean (20 SMA).

• Alert States:

Over-Extended (> 2.0 SD): Warning that price is statistically likely to revert to the mean (Elastic Snap-back), even if the trend remains technically valid. New entries are discouraged in this zone.

Normal: Price is within standard distribution limits, suitable for trend-following entries.

D. Volatility Regime Classification

• Metric: Compares current ATR against a 100-period historical baseline to categorize the market state.

• Regimes:

Low Volatility (Lvl < 1.0): Market Compression. Often precedes volatility expansion events.

Mid Volatility (Lvl 1.0 - 1.5): Standard operating environment.

High Volatility (Lvl > 1.5): Elevated market stress. Risk parameters should be adjusted (e.g., reduced position size) to account for increased variance.

E. Performance Telemetry

• Function: Displays the historical reliability of the Trend Baseline for the current asset and timeframe.

• Operational Threshold: If the displayed Win Rate falls below 40%, it suggests the current market behavior is incoherent (choppy) and does not respect trend logic. In such cases, switching assets or timeframes is recommended.

Operational Protocols & Signal Decoding

Visual Interpretation Standards

• Laminar Flow (Trade Confirmation): A valid trend is visually confirmed when the 15-layer SMA Ribbon is fully expanded and parallel. This indicates distributed momentum across timeframes.

• Consolidation (No-Trade): If the ribbon appears twisted, knotted, or compressed, the market lacks a unified directional vector.

• Baseline Interaction: The Triple-Smoothed Baseline acts as a dynamic support/resistance filter. Long positions remain valid only while price sustains above this structure.

System Calibration (Settings)

• Adaptive Signal Filtering (Prev. Anti-Greed): Enabled by default. This logic automatically raises the required trend slope threshold following consecutive wins to mitigate behavioral bias.

• Impulse Sensitivity: Controls the reactivity of the Volatility Core. Higher settings capture faster moves but may introduce more noise.

⚙️ Chapter 6: System Configuration & Alert Guide

This section provides a complete breakdown of every adjustable setting within Impulse Reactor to assist you in tailoring the engine to your specific needs.

🌐 LANGUAGE SETTINGS (Localization)

◦ Select Language (Default: English):

Function: Instantly translates all chart labels, dashboard texts into your preferred language.

Supported: English, Korean, Chinese, Spanish

⚡ IMPULSE CORE SETTINGS (Volatility Engine)

◦ Deviation Lookback (Default: 30): The period used to calculate the standard deviation of volatility.

Role: Sets the baseline for normalizing momentum. Higher values make the core smoother but slower to react.

◦ Fast Pulse Length (Default: 10): The short-term ATR period.